Why Downside Protection ETFs Fall Short for Young Healthcare Professionals—and Smarter Ways to Balance Risk and Growth

Why Downside Protection ETFs Fall Short for Young Healthcare Professionals—and Smarter Ways to Balance Risk and Growth

Disclaimer: Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal.

As a physician, dentist, or other healthcare professional beginning your career, building a robust investment portfolio is critical for your long-term financial health. The market offers a range of products promising “downside protection,” including a popular group of downside protection ETFs. These funds aim to cap losses in a downturn while still participating modestly in market gains. But do they truly deliver the protection and growth you need? In most cases, the answer is no.

In this in-depth guide, we’ll explore:

How downside protection ETFs work

Why they often underdeliver for young professionals

Cost, complexity, and hidden drawbacks

Traditional strategies that may serve you better

Steps to build a balanced, growth-oriented portfolio

1. What Are Downside Protection ETFs?

Downside protection ETFs (also called “buffer ETFs” or “defined outcome ETFs”) use options and derivatives to create a floor under losses—typically at the expense of capping upside returns. In a given 12-month period, these funds may limit your loss to, say, 10%, while also capping your gain at 6% or 7%. The theory is appealing: reduce extreme losses without giving up all market participation.

Key features:

Buffered downside loss in a defined period

Capped upside return, usually around 6–7%

Rolling annual windows or fixed terms

Option-based strategies requiring active rollovers

However, data shows these caps bite hard: 58% of 12-month S&P 500 returns exceed 7%—meaning you miss out on the majority of positive years. And while 71% of rolling windows are positive, you sacrifice material upside for limited downside relief.

2. Why Young Healthcare Professionals Are Drawn to “Protected” ETFs

Physicians and dentists often carry substantial student debt, variable compensation, and delayed peak earning years. Naturally, the promise of “safeguarding” your first significant investments is tempting. You want:

Peace of mind when markets swing wildly

Preservation of capital for short-term goals (residency start, down payment)

Exposure to equities for long-term growth

Downside protection ETFs market directly to risk-averse investors, touting simplicity and the allure of “set it and forget it” protection. But the reality is more nuanced—and often underwhelming.

3. The Hidden Costs and Complexities

3.1 Expense Ratios and Trading Costs

These ETFs typically charge higher expense ratios—often 0.50% to 1.00%—to cover option premiums and strategy fees. Compare that to broad market index ETFs at 0.03% to 0.10%. Over decades, those extra basis points compound to tens of thousands of dollars in eroded returns.

3.2 Timing and Rollover Risk

The protection works only if you hold from the designated start date to the end date. Buying “mid-cycle” means you pay for protection you can’t fully reap. Market moves between roll dates can leave you under-protected or over-paying for options that have already drifted.

3.3 Opportunity Cost of Capped Gains

In strong bull markets, your upside limit kicks in early. Historical data: 58% of rolling 12-month S&P periods exceed a 7% gain. By capping that, you sacrifice substantial compound growth—precisely what young investors need most.

4. Comparing to Traditional Risk Management Strategies

Rather than complex buffers, many advisors recommend straightforward diversification:

Equities (U.S., international, small cap, sector tilts)

Fixed income (Treasuries, investment-grade bonds, TIPS)

Alternative assets (real estate, commodities, real-asset funds)

Regular rebalancing to target allocations

Why these often outperform “protected” ETFs over time:

Lower fees and transparent holdings

No hidden timing requirements

Consistent exposure to market gains

Ability to tailor risk using bond ladders, duration management

5. Smarter Alternatives for Young Healthcare Professionals

5.1 Target-Risk Portfolios

A diversified mix of stocks and bonds matched to your risk tolerance. Rebalance annually to maintain your desired allocation. This simple approach has beaten many fancy structures over the long run.

5.2 Bond Ladders for Short-Term Goals

For dollars earmarked for a home down payment or expected tuition, build a series of short-to-medium-term bonds or CDs. You gain predictable income and principal return without equity volatility.

5.3 Tax-Efficient Retirement Accounts

Maximize your 401(k)/403(b), IRA, or Roth IRA to shelter growth from taxes. Equity-heavy allocations here compound faster when left to grow tax-free or tax-deferred.

5.4 Dollar-Cost Averaging and Automatic Investing

Consistent contributions smooth out volatility. You buy more shares when prices fall, fewer when they rise. Over decades, this disciplined habit can reduce risk without sacrificing growth.

6. Building Your Customized Plan

No two healthcare careers are identical. Your plan should reflect:

Current debt levels and repayment schedules

Short-term liquidity needs (residency, relocation, startup costs)

Long-term goals (early retirement, practice buy-in, legacy planning)

Risk tolerance and time horizon

At Mainstay Capital, our process begins with understanding your unique situation. From there, we craft a diversified strategy grounded in low-cost ETFs, bonds, and alternatives—no unnecessary complexity or hidden caps.

7. Step-by-Step Implementation

Define your goals: short, medium, and long term.

Assess your risk tolerance honestly.

Choose low-cost broad market ETFs for equities.

Build a bond ladder or select diversified bond funds.

Consider alternative allocations (real assets, private markets) if suitable.

Automate contributions and rebalance at predetermined intervals.

Review annually or upon life changes (promotion, practice sale).

Need help? Learn more about our services and how we guide young healthcare professionals toward financial confidence.

8. Conclusion

Downside protection ETFs may sound appealing, but their capped upside, higher fees, and timing pitfalls often leave young investors worse off over the long run. For most physicians and dentists just starting out, simple diversification, bond ladders for short-term goals, and disciplined contributions provide more growth potential and fewer surprises.

Your financial future deserves more than a promise of limited loss and capped gain. It needs a clear plan, low costs, and a portfolio built around your goals. Discover how Mainstay Capital can help you chart the path toward lasting financial health—no complex buffers required.

Disclaimer: Investing involves risk, including possible loss of principal. Consult your advisor before making investment decisions. Past performance is not indicative of future results.

© 2025 Mainstay Capital. All rights reserved.

The Ultimate Financial Blueprint for Young Healthcare Professionals

The Ultimate Financial Blueprint for Young Healthcare Professionals

Starting your career as a dentist or physician is exciting—but it also brings unique financial challenges. From juggling student loan payments and 1099 taxes to planning for retirement and someday owning a practice, there’s a lot to tackle. This guide offers a clear, step-by-step plan to help young healthcare professionals master their finances, build lasting security, and pursue practice ownership with confidence.

Key topics: tax planning for doctors, dentist student loan management, retirement planning for healthcare professionals, fiduciary financial advisor for doctors.

1. Understanding Your Financial Starting Point

Every strong financial plan begins with an honest look at where you stand today. Take time to gather your numbers and commit to tracking them regularly.

1.1 Budgeting and Cash Flow

• List all income sources (W-2 salary, 1099 contractor work, side gigs).

• Track monthly expenses: rent or mortgage, utilities, groceries, insurance, student-loan payments, practice expenses (if any).

• Aim for a simple zero-based budget—every dollar is assigned a purpose.

1.2 Student Loan Snapshot

Outline each loan: remaining balance, interest rate, repayment plan (e.g., income-driven repayment, public student loan forgiveness), and monthly payment. A clear picture helps you compare strategies like refinancing versus staying on an income-driven plan.

1.3 Tax Profile

If you’re a 1099 contractor or part owner of a practice, you must handle quarterly tax filings. Even if you’re W-2, additional income streams can complicate your tax picture. Starting early gives you more time to optimize deductions, retirement contributions, and potential entity structures.

2. Mastering Tax Planning for Doctors

Effective tax planning can save thousands annually. Here’s how to get started:

2.1 Quarterly Estimated Taxes

If you receive 1099 income or have side revenue, calculate your estimated tax payments each quarter. Tools like IRS Form 1040-ES worksheets or online calculators can help. Underpaying leads to penalties; overpaying ties up cash you could invest.

2.2 Business Entity Considerations

Operating as an S-corporation or LLC may offer tax benefits. Earnings distributed as dividends can avoid self-employment tax. Work with a qualified CPA or an fiduciary financial advisor for doctors to weigh the costs and complexity.

2.3 Maximizing Deductions

Retirement contributions (401(k), SEP IRA, SIMPLE IRA)—reduce taxable income.

Business expenses—home office, CME courses, professional dues, malpractice insurance.

Health savings account (HSA) contributions if you have a high-deductible health plan.

Keep thorough receipts and log business mileage automatically with an app.

3. Conquering Student Loan Management

Student debt can feel overwhelming. But with a tailored student loan management plan, you can reduce interest costs and gain peace of mind.

3.1 Income-Driven Repayment vs. Refinancing

Income-driven plans cap your payment based on your discretionary income—often 10%–15%. If you expect loan forgiveness (Public Service Loan Forgiveness or 20-year forgiveness), staying on that track makes sense. If you have solid cash flow, refinancing at a lower interest rate could save money but forfeits federal protections.

3.2 Forgiveness Programs

Public Service Loan Forgiveness (PSLF)—available after 120 qualifying payments for government or nonprofit employers.

State-specific programs—some states offer loan repayment assistance for practice in underserved areas.

20 years of payments on an Income Driven Repayment program may result in forgiveness of the remaining loan balance.

3.3 Prepayment Strategies

If you aim to pay off debt aggressively, apply extra payments to the principal on the highest-rate loans first. Automate an additional fixed amount monthly to reduce your balance faster.

4. Building a Solid Retirement Plan

Even early-career physicians and dentists should prioritize retirement planning. Time is your greatest ally when compounding growth is on your side.

4.1 Retirement Account Options

401(k) or 403(b) through your employer—max out any matching contributions first.

Individual Retirement Accounts (Traditional IRA or Roth IRA)—consider Roth if you expect higher tax rates later.

SEP IRA or Solo 401(k) if you have side income or run a small practice.

4.2 Asset Allocation Basics

Young professionals can afford a growth-oriented mix, then gradually shift toward more conservative allocations as you near practice ownership or retirement.

4.3 Catch-Up Contributions

Once you turn 50, you can make catch-up contributions in addition to the annual limit. Plan ahead so you’re ready to boost savings when the time comes.

5. Planning for Practice Ownership

Owning your own dental or medical practice can be rewarding—but it requires careful financial and operational planning.

5.1 When to Consider Ownership

• You have stable cash flow and a solid credit history.

• You understand local market demand and have a clear business plan.

• You’re prepared for upfront costs: real estate, equipment, staffing.

5.2 Financing Your Practice

Bank loans or SBA loans—competitive rates but strict underwriting.

Seller financing—may require higher interest but fewer upfront costs.

Partner buy-ins—pool resources with colleagues to lower individual debt.

5.3 Practice Management Consulting

Expert guidance can streamline billing, staffing, and compliance. Explore our Our Process page to see how we help healthcare clients launch and grow practices.

6. Risk Management and Insurance

Protecting your income and loved ones is a vital part of your financial blueprint.

6.1 Term Life Insurance

Term policies offer high coverage at low cost. As your income grows, you can layer on additional policies to match evolving needs.

6.2 Disability Insurance

A top-priority for physicians and dentists—covering 50%–60% of your gross income if illness or injury prevents you from working.

6.3 Malpractice and Liability

Ensure you have adequate malpractice coverage, especially if you’re transitioning to private practice ownership. Umbrella liability policies can provide an extra layer of protection.

7. Why Choose a Fiduciary Advisor?

Working with a fiduciary financial advisor ensures your interests come first. Here’s what to expect when you partner with us:

Transparent Fees: $1,200 onboarding + $2,400/year. Asset management is free under $200K, 0.3% over $200K.

Comprehensive Services: Quarterly check-ins, on-call support, detailed analyses of taxes, student loans, investments, and insurance.

Structured Process: Four onboarding meetings covering organization, goals, risk management, and customized recommendations.

Ethical Standards: As a CFP®, MBA, and IRS Enrolled Agent, we follow strict standards of conduct and avoid conflicts of interest.

Disclaimer: This information is educational only and does not constitute personalized advice. Past performance does not guarantee future results.

8. Creating Your Personalized Financial Blueprint

Pulling it all together, your financial blueprint should include:

A clear budget and cash-flow plan updated monthly.

Quarterly tax payment schedule with entity-structure reviews.

Student loan strategy aligned with your career path.

Retirement account setup and target asset allocation.

Insurance coverage to protect income and family.

Timeline and criteria for practice-ownership decisions.

9. Next Steps

You don’t have to navigate your financial journey alone. Schedule a free discovery call today to explore how we can help you build and execute your personalized financial plan.

Schedule Your Call

Questions? Contact us directly at marcus.miller@mainstay-capital.com or call 813-699-9317.

© 2025 Mainstay Capital. All rights reserved. Disclaimer: This content is for educational purposes only. Please consult a qualified financial professional before making any decisions.

7 Financial Strategies for Early-Career Healthcare Professionals

7 Financial Strategies for Early-Career Healthcare Professionals

Embarking on a medical or dental career is an exciting milestone, but the financial landscape you inherit can feel complex. From managing student loans to planning for private practice growth, early-career physicians and dentists face unique challenges. At Mainstay Capital, we’ve guided healthcare professionals through these critical years. In this comprehensive guide, you’ll discover seven practical strategies—rooted in real-world experience—to align your vision, stabilize cash flow, and set a sustainable path for long-term success.

1. Clarify Your Vision and Core Values

Before diving into spreadsheets or investment products, take a moment for self-reflection. What motivates you? Family stability, community impact, early retirement, or philanthropic goals might top your list. Aligning financial planning with your personal and professional values ensures every decision supports your larger mission.

Why Values-Driven Planning Matters

Provides clear direction for budgeting, saving, and investing.

Helps set realistic expectations for practice ownership or partnership.

Minimizes decision fatigue when facing unexpected financial challenges.

Action Steps

Host a vision-setting session: Write down your top five personal and professional objectives.

Rank values by urgency: Consider what matters most in the next 1, 5, and 10 years.

Document a preliminary “Financial Mission Statement” to guide all future plans.

2. Build a Robust Cash Flow and Budget Plan

Effective cash flow management is the bedrock of financial stability for early-career healthcare professionals. Whether you’re earning your first attending salary or billing patients in private practice, understanding inflows and outflows will empower smarter decisions.

Key Components of a Healthcare Professional Budget

Fixed Expenses: Rent or mortgage, insurance premiums, loan payments.

Variable Expenses: Continuing education, medical equipment, travel.

Deferred Goals: Emergency fund accumulation, retirement contributions.

Tools and Techniques

Adopt specialized budgeting software tailored to physicians and dentists.

Schedule a quarterly “finance check-in” to adjust projections after seasonality or practice growth.

Automate savings: Allocate a portion of every deposit to emergency reserves and retirement accounts.

For an in-depth walkthrough of our cash flow process, visit our Our Process page.

Compliance note: All recommendations are illustrative. Your results may vary based on individual circumstances. Past performance does not guarantee future returns.

3. Tackle Student Loans and Debt Strategically

Medical and dental school debts often eclipse six figures. While income-driven repayment or refinancing can offer relief, a tailored strategy will minimize total interest and help you reach financial independence sooner.

Debt-Reduction Strategies

Evaluate Repayment Options: Public Service Loan Forgiveness, income-driven plans, hybrid strategies.

Refinancing Considerations: Look for competitive rates, flexible terms, and potential tax deductions.

Snowball vs. Avalanche: Choose a payoff method that aligns with your psychological and financial goals.

Professional Tax Planning

Maximize above-the-line deductions for student loan interest.

Structure your professional entity—LLC or S-corp—for optimal tax efficiency.

Plan charitable giving and retirement contributions to reduce taxable income.

Your debt payoff timeline should sync with personal goals—starting a family, purchasing a home, or opening a practice. For guidance on entity structuring and tax-smart strategies, explore our Services.

Compliance note: Mainstay Capital does not provide legal advice. Consult a professional advisor before implementing legal strategies.

4. Finance Your Private Practice or Partnership Entry

Transitioning from employee to practice owner or equity partner brings both freedom and financial risk. Structured planning around financing, overhead, and growth milestones is essential to avoid cash crunches.

Financing Options

Conventional Bank Loans: Industry-specific lenders often offer favorable terms for healthcare professionals.

Equipment Leasing: Preserve capital by leasing high-cost diagnostic or dental equipment.

Physician-Specific Programs: Investigate association-based loan forgiveness or low-interest credit lines.

Controlling Overhead and Scalability

Leverage technology to automate patient billing and appointment scheduling.

Adopt a lean staffing model early; cross-train staff to handle multiple functions.

Implement scalable workflows that allow adding providers without exponential cost increases.

For a blueprint on practice financing and scalable infrastructure, learn more via our Services offerings.

Compliance note: Investment strategies involve risk. There is no guarantee that any investment or strategy will be suitable or profitable.

5. Plan for Sustainable Growth and Succession

As your practice matures, shifting responsibilities to associates or partners becomes vital. Thoughtful succession planning ensures client continuity and preserves the firm’s legacy.

Developing Your Team

Create clear career pathways and compensation models for emerging providers.

Implement regular performance reviews and a structured feedback loop.

Offer mentorship programs to transfer client relationships smoothly.

Succession Roadmap

Draft a multi-phase transition timeline: from first referral handoff to full autonomy.

Establish governance policies and decision-making protocols.

Handle equity transitions with clear valuation metrics and buy-sell agreements.

Curious about our approach? Visit the About Us page to see our team’s background in guiding practice transitions.

6. Balance Personal Milestones with Financial Goals

Your life outside the clinic—family, health, hobbies—should thrive alongside your financial plan. Overcommitment can erode both your well-being and your bottom line.

Integrating Personal and Professional Plans

Create a “life calendar” marking events like weddings, children, or sabbaticals.

Allocate savings and insurance coverage—disability, life, health—to protect loved ones.

Set aside time and budget for self-care and continuing education.

Wellness and Financial Therapy

Consider financial coaching or therapy to align mindset and money behaviors.

Track non-financial metrics—sleep, exercise, stress levels—to optimize performance.

Reassess your vision periodically to avoid burnout and maintain fulfillment.

7. Next Steps: Build Your Customized Financial Roadmap

Implementing these seven strategies will position you for sustained success—both financially and personally. Whether you’re an attending physician, a newly minted dentist, or a practice partner, our team at Mainstay Capital is ready to guide you every step of the way. Visit our Our Process page to schedule a complimentary discovery call and begin crafting a plan tailored to your unique goals.

Thank you for trusting us as your fiduciary partner. We look forward to supporting your journey from early-career ambitions to enduring freedom and impact.

© 2025 Mainstay Capital. All Rights Reserved. Mainstay Capital is a Registered Investment Advisor. Advisory services are offered only to clients or prospective clients where Mainstay Capital and its representatives are properly licensed or exempt from licensing.

Investing involves risk, including the potential loss of principal. Past performance is not indicative of future results. This blog post is for informational purposes and does not constitute an offer to sell or a solicitation of an offer to buy any security.

How Cyborg Financial Advisors Are Transforming Wealth Management for Young Healthcare Professionals

How “Cyborg” Financial Advisors Are Transforming Wealth Management for Young Healthcare Professionals

As a physician, dentist, or allied health professional starting your career, you juggle demanding schedules, ongoing education, and the responsibility of patient care. Amidst this whirlwind, planning your financial future can feel overwhelming. Enter the “cyborg” financial advisor: a hybrid approach that combines advanced AI-powered tools with human empathy and judgment. In this post, we’ll explore how this model can help you optimize cash flow, manage student loan debt, and build long-term wealth—without sacrificing the personalized touch you value.

By understanding the intersection of AI in financial planning and traditional advisory services, you’ll see how automated projections, stress-tested scenarios, and real-time insights can integrate seamlessly with a trusted advisor’s guidance. Let’s dive in.

1. The Rise of AI in Financial Planning

Financial technology (fintech) has evolved rapidly over the last decade. Tools once limited to large institutions are now accessible to individual advisors and their clients. Among these innovations, digital wealth solutions and predictive analytics stand out by providing:

- Automated cash-flow projections that model income fluctuations, expenses, and savings targets.

- Scenario stress tests that simulate market downturns, inflation changes, and life events like buying a home or starting a family.

- Real-time portfolio monitoring that flags rebalancing opportunities and potential tax-saving maneuvers.

Why AI Alone Isn’t Enough

While AI excels at number crunching and pattern recognition, it can’t fully grasp the psycho-emotional factors guiding your decisions. For instance, your risk tolerance isn’t merely a percentage—it’s shaped by experiences, values, and personal goals. A purely algorithmic plan might miss nuances such as:

- Your desire to reduce student loan debt quickly versus funding retirement.

- Emotional comfort with market volatility.

- The legacy you wish to leave for family or charitable causes.

This is precisely why the cyborg advisor model is gaining ground: it leverages AI’s computational power while preserving human empathy and strategic judgment.

2. Why Young Healthcare Professionals Need Holistic Financial Advice

Medical school tuition, residency stipends, and licensing fees add up quickly. Many young physicians and dentists graduate with substantial debt while also tackling high living expenses. A holistic approach considers:

- Debt management strategies to prioritize high-interest loans or explore refinancing options.

- Income optimization through tax-efficient structures, practice ownership, or side services.

- Insurance planning to protect against disability, liability, and malpractice claims.

- Retirement roadmaps that align contributions to IRAs, 401(k)s, or 403(b)s based on your career stage.

- Personal goals such as homeownership, family planning, or philanthropy.

Integrating AI tools within this framework lets advisors generate customized projections in minutes—rather than days—so you can see the impact of each decision immediately. But it also requires a trusted human partner to interpret these projections in light of your unique circumstances.

Ready to explore a holistic financial strategy? Learn more about Our Process to see how we combine technology with personalized guidance.

3. Understanding the Cyborg Advisor Model

The term “cyborg advisor” evokes a seamless synergy between machine intelligence and human insight. Here’s how it works in practice:

- Data Integration: Your advisor gathers financial data—bank accounts, loans, insurance policies—into a central planning platform. Automated AI note-taking captures meeting highlights and action items.

- Predictive Modeling: AI algorithms generate multiple “what-if” scenarios, from aggressive debt repayment to maximum retirement savings. These projections update in real time as assumptions change.

- Interactive Review: In a collaborative session, you and your advisor evaluate the scenarios. Your advisor asks structured questions to surface hidden values and adjust assumptions.

- Empathy-Driven Coaching: Your advisor translates technical outputs into relatable insights. Whether you’re anxious about market dips or unsure about practice ownership, they provide context and reassurance.

- Ongoing Monitoring: AI tools continuously scan for tax-saving opportunities, portfolio rebalancing triggers, and changes in your financial profile. Your advisor reviews critical alerts and recommends adjustments.

This approach offers the best of both worlds: the speed and accuracy of machine calculations plus the compassion and expertise of a dedicated professional. For young healthcare workers building their careers, this can be a game-changer.

4. Integrating AI Tools for Physicians, Doctors, and Dentists

Not all AI solutions are created equal. Here’s a look at the key categories and how they benefit healthcare professionals:

1. Financial Planning Software

Platforms like robust wealth management suites generate detailed cash-flow analyses and retirement projections. They allow advisors to:

- Run complex Monte Carlo simulations in seconds.

- Visualize retirement readiness with intuitive charts.

- Model practice buy-in or partnership transitions.

2. AI-Powered CRMs

Client Relationship Management systems with AI note-takers and meeting transcriptions streamline communication:

- Automatic follow-up reminders for key deadlines.

- Sentiment analysis to gauge client satisfaction.

- Data tagging for personalized outreach campaigns.

3. Middleware AI Assistants

These “behind-the-scenes” tools connect disparate systems—bank accounts, billing software, investment platforms—and feed unified data into planning dashboards.

Among these, financial planning software often takes center stage by delivering the most accurate projections. However, only a skilled advisor can interpret those results in light of your psycho-emotional drivers.

Interested in a technology-enhanced advisory experience? Discover our full Services tailored to healthcare professionals.

5. Steps to Build Your Personalized Financial Plan

Whether you’re fresh out of residency or a few years into practice, follow these five key steps:

- Clarify Your Goals: Do you plan to purchase a home, start a family, or launch a specialty practice? Document short- and long-term objectives.

- Consolidate Data: Aggregate your loan statements, investment accounts, insurance policies, and monthly budget.

- Leverage AI Projections: Use planning software to simulate different strategies—aggressive debt payoff, maxing retirement contributions, or diversifying investments.

- Align With Your Values: Partner with an advisor to interpret results and ensure the plan reflects your comfort level and broader life mission.

- Implement and Monitor: Automate savings, tax-loss harvesting, and portfolio rebalancing. Schedule quarterly check-ins to review AI-driven alerts and adjust as needed.

Curious about how we guide young professionals through this process? Learn more on our About Us page, then schedule a complimentary discovery call from our Homepage.

6. Overcoming Common Financial Challenges in Healthcare

Healthcare professionals often face unique obstacles: high debt loads, irregular income early in practice, and exposure to liability risks. Here’s how the cyborg advisor model addresses them:

- Student Loan Management: AI can rank loans by interest rate, suggest refinancing, or propose alternative repayment plans. Your advisor then compares pros and cons based on your career trajectory.

- Variable Income Smoothing: Predictive analytics forecast cash-flow gaps during fellowship or partnership buy-in. Automated budgeting tools keep you on track even when earnings fluctuate.

- Risk Mitigation: Machine learning flags potential shortfalls in disability or malpractice coverage. Your advisor works with insurance specialists to close any gaps.

- Tax Efficiency: AI-driven tax-planning modules identify deductions unique to medical professionals—continuing education, licensing fees, or home office expenses.

By pairing these AI insights with human expertise, you gain a comprehensive defense against financial stressors that can derail long-term wealth building.

Conclusion: Embracing the Future of Healthcare Wealth Management

The “cyborg” financial advisor model isn’t science fiction—it’s the next frontier in wealth management for young healthcare professionals. By blending AI’s predictive horsepower with the empathy and strategic vision of a human advisor, you get a financial plan that’s accurate, adaptive, and deeply personalized.

If you’re ready to experience this powerful synergy, visit MainStay Capital today. Our team specializes in financial planning for physicians, dentists, and allied healthcare professionals. Let us help you take control of your financial future—so you can focus on what you do best: caring for patients.

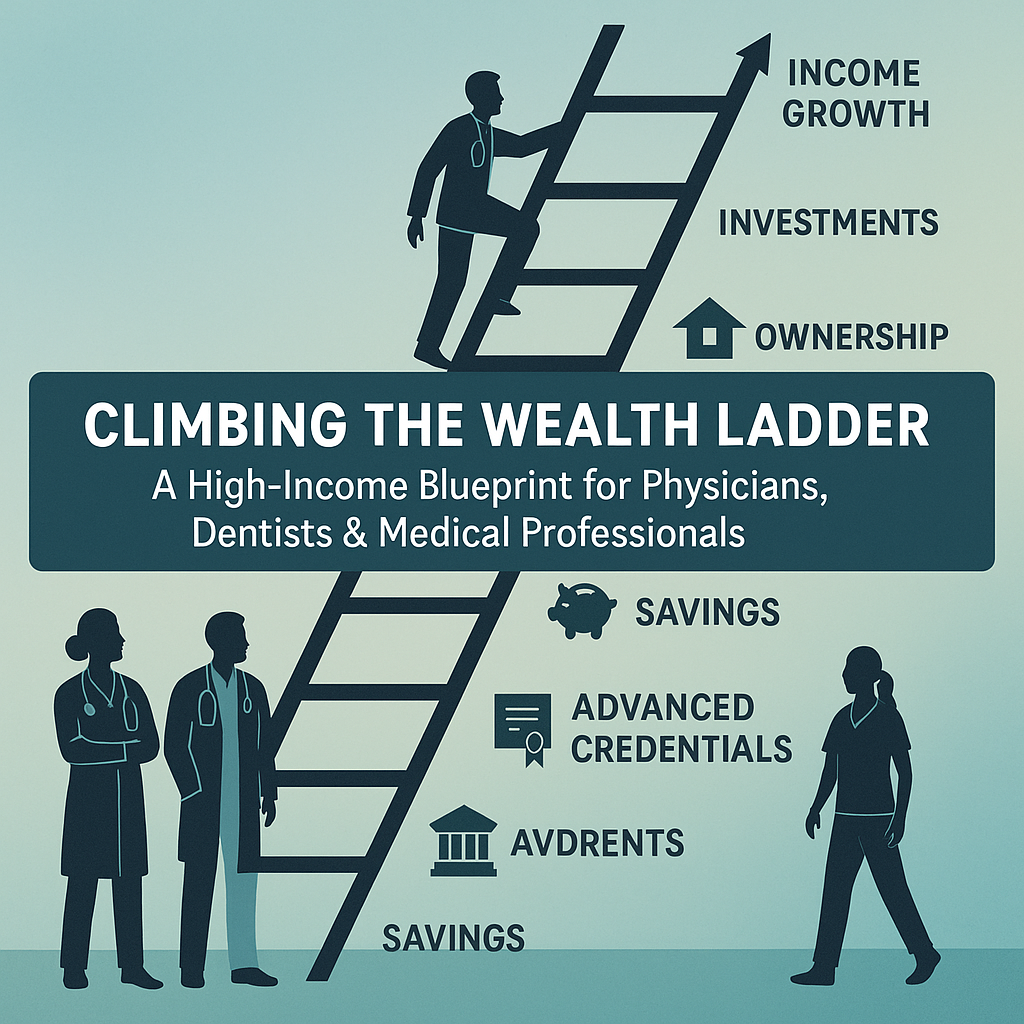

Climbing the Wealth Ladder: A High-Income Blueprint for Physicians, Dentists & Medical Professionals

Climbing the Wealth Ladder: A High-Income Blueprint for Physicians, Dentists & Medical Professionals

As a busy physician, dentist, or clinician, you’ve invested years honing your technical skills, earning degrees, and caring for patients. Yet when it comes to money, the path to building enduring wealth can feel uncertain. Does higher income automatically translate into a comfortable retirement? Which strategies move the needle fastest? In this comprehensive guide—tailored for medical professionals like you—we unpack why income today is the best leading indicator of wealth tomorrow, explore four high-impact income-growth paths, and lay out an actionable plan to climb your personalized “Wealth Ladder.”

Why Income Matters More Than You Think

Conventional personal finance advice often emphasizes budgets, spending discipline, and “mindset.” While important, empirical research shows that for working-age households, current income is the strongest predictor of future net worth. Data from long-running studies (such as the Panel Study of Income Dynamics) demonstrate:

Households in the top quintile of income in a given decade move to the top wealth quintile a decade later over 70% of the time.

High-income earners rarely end up with low net worth, provided they avoid extreme spending or leverage risks.

Conversely, modest incomes make it statistically harder to accumulate substantial assets, even with disciplined saving.

For medical professionals who often command above-average salaries, the opportunity is clear: focus on income growth to accelerate wealth creation, rather than relying solely on expense cutting or financial “mindset” shifts.

The Four Paths to Higher Income

Drawing on both academic findings and real-world case studies, experts identify four core ways to boost earnings:

Sales & Persuasion

In the medical context, sales skills translate to effective patient communication, negotiation of fee schedules, and physician leadership roles that come with performance-linked compensation.

Negotiating higher reimbursement rates with insurers or hospital systems

Leading high-value service lines (e.g., orthopedic sports medicine, cosmetic dentistry)

Developing referral networks and building specialty clinics

Technical & Analytical Expertise

Your clinical proficiency—whether robotic surgery, implant dentistry, or interventional radiology—is a high-value skillset that remains in demand despite automation trends. Consider sub-specialty fellowships or certifications that command premium billing codes.

Advanced Degrees & Credentials

Data shows that additional credentials—MBA, MPH, JD, or advanced clinical fellowships—can yield significant income boosts over time:

An MBA may unlock health system leadership roles or private equity opportunities in healthcare.

Joint MD/MBA programs often lead to executive director or C-suite positions.

Board certifications in high-margin specialties increase negotiating power.

Ownership Stakes

Equity ownership—whether in a private medical practice, dental clinic, or healthcare startup—offers exponential upside:

Partner shares in a group practice can yield distributions beyond salary.

Stock options in medical device or digital health firms align your clinical expertise with startup growth.

Franchise or multi-location dental models multiply earnings and resale value.

The “Wealth Ladder” Framework: From Income to Assets

The concept of a “Wealth Ladder” illustrates how you convert higher earnings into lasting net worth. Climbing each rung requires disciplined allocation of surplus income:

Save & Build Reserves: Maintain 6–12 months of expenses in liquid form—emergency fund and operating reserves for private practices.

Optimize Tax Efficiency: Max out retirement vehicles (401(k), 403(b), SEP-IRA) and leverage Section 179 for equipment depreciation.

Invest in Core Portfolios: Diversify across low-cost equities, bonds, and real estate investment trusts (REITs).

Expand Ownership: Reinvest practice profits into new service lines or physical expansions.

Legacy Planning: Implement trusts, buy-sell agreements, and insurance strategies to protect family wealth.

Every additional dollar of income can be deliberately directed up these rungs to multiply your long-term net worth.

Actionable Steps to Boost Your Income

Inventory Your Skills: Chart your clinical competencies, leadership abilities, and market demand gaps.

Set Income Targets: Define a 3- to 5-year earnings goal aligned with your desired net worth outcome (e.g., $500K base + $150K bonuses).

Develop a Credentials Roadmap: Plan fellowships, board certifications, or advanced degrees with clear ROI projections.

Negotiate Smart: Use benchmark data (MGMA, ADA surveys) when renegotiating compensation or partnership terms.

Explore Ownership: Evaluate practice valuations, partnership models, and potential startup co-founder roles.

Automate Savings: Schedule monthly transfers into tax-advantaged retirement, HSA, and brokerage accounts.

Review & Adjust Quarterly: Track income growth, net worth progression, and pivot as needed.

Integrating with Mainstay Capital

At Mainstay Capital, we partner with ambitious healthcare professionals to turn high income into enduring wealth. Our four-step process ensures your path is tailored, efficient, and compliant with fiduciary best practices:

Our Process: Strategy discovery, customized planning, implementation, and ongoing monitoring.

Services: Wealth planning, retirement strategies, tax optimization, risk management, and practice succession.

About Us: Meet our CFP® professionals and investment specialists dedicated to healthcare clients.

Ready to translate your hard-earned income into lifelong wealth? Contact us to schedule a complimentary discovery session.

Frequently Asked Questions

1. Why can’t I just save more and stop worrying about income?

While frugal habits help, data shows that savings rates alone cannot overcome low or stagnant earnings over decades. Expanding your income floor broadens the base from which you save and invest.

2. What if I’m already burdened with medical school debt?

High-interest loans can erode your ability to build wealth. Consider refinance strategies, income-driven repayment while you ramp up earnings, and accelerated payment plans once you hit new salary milestones.

3. How do I balance work–life with extra credentialing?

Frame credentialing as an investment. A carefully chosen fellowship or MBA program can pay for itself within 3–5 years via higher compensation and leadership roles.

Key Takeaways

Current income is the strongest leading indicator of future wealth for working professionals.

Focus on at least one of the four high-impact income paths: sales & persuasion, technical expertise, advanced credentials, or ownership stakes.

Allocate surplus income up the Wealth Ladder: reserves, tax-efficient retirement, diversified investments, and practice growth.

Review progress quarterly and adjust your strategy to stay on track toward your net worth goals.

Partner with fiduciary advisors who understand the unique needs of physicians, dentists, and healthcare leaders.

Disclosure & Compliance

Mainstay Capital, LLC (“Mainstay Capital”) is a registered investment adviser. This content is for informational purposes only and does not constitute investment advice or an offer to sell securities. Past performance does not guarantee future results. Investing involves risk, including the loss of principal. Please consult your financial, tax, and legal advisors before making any investment or planning decisions.

© 2025 Mainstay Capital, LLC. All rights reserved.

The Separate + Joint Method: A Modern Approach to Managing Marriage Finances for Young Healthcare Professionals

“`html

The Separate + Joint Method: A Modern Approach to Managing Marriage Finances for Young Healthcare Professionals

Marriage marks a significant milestone not just emotionally but financially. As young healthcare professionals—whether you’re physicians, dentists, pharmacists, physical therapists, or psychologists—the way you manage money with your spouse can set the foundation for your shared future. Balancing demanding careers with personal lives leaves little room for financial discord. Enter the Separate + Joint Method: a strategy that fosters both collaboration and independence in managing married finances.

Understanding the Financial Nuances of Healthcare Professionals

The financial landscape for healthcare professionals is unique. With substantial student loans, fluctuating incomes during residencies, and the eventual upswing in earnings, planning becomes crucial. Doctors and dentists often start their careers later, accumulating debt before reaping the financial rewards of their professions. Pharmacists and physical therapists might have more stable entry-level incomes but still face significant educational expenses.

Amidst these challenges, merging finances in marriage adds another layer of complexity. It’s essential to find a system that respects individual financial journeys while promoting a unified approach to shared goals.

Why Traditional Methods Might Not Suffice

Traditional financial arrangements in marriage typically fall into three categories:

- Fully Joint Accounts: All funds are pooled together, offering complete transparency but potentially limiting individual autonomy.

- Completely Separate Accounts: Each spouse manages their finances independently, which can lead to a lack of coordination on joint expenses and goals.

- Hybrid Models: A mix of joint and separate accounts, but without a structured approach, often leading to confusion.

For healthcare professionals, these methods might not address specific needs like managing student debt, investing in career advancement, or supporting extended family members.

Introducing the Separate + Joint Method

The Separate + Joint Method combines the best of both worlds—maintaining personal financial independence while collaborating on shared expenses and goals. Here’s how it works:

- Maintain Separate Pre-Marriage Assets: Assets acquired before marriage remain individually controlled. This respects the financial foundations each person built independently.

- Establish Separate Personal Accounts: Both spouses keep personal accounts for individual expenses and discretionary spending.

- Create a Joint Account for Shared Expenses: A joint account acts as the financial hub for household expenses, mortgage or rent, utilities, groceries, and joint investments.

- Income Allocation: Both partners deposit their incomes into the joint account, from which shared expenses are paid. Surplus funds can be left in the joint account, equally divided into personal accounts, or allocated towards joint financial goals.

Benefits of the Separate + Joint Method

Implementing this method offers several advantages:

Financial Transparency

With a joint account for shared expenses, both partners have visibility into household spending. This transparency builds trust and ensures that both are on the same page regarding financial priorities.

Preservation of Financial Independence

Maintaining separate accounts allows each spouse to manage personal expenses without feeling scrutinized. This is particularly empowering for individuals who value autonomy over their finances.

Equitable Contribution and Access

By agreeing on how to handle surplus funds and deficits, the method promotes fairness. Personal withdrawals from the joint account require matched amounts, ensuring that both partners benefit equally.

Adaptability for Individual Needs

Non-shared expenses, like supporting family members or pursuing personal interests, are managed through individual accounts. This flexibility is crucial for professionals who might have unique financial obligations.

Implementing the Separate + Joint Method: A Step-by-Step Guide

1. Open the Necessary Accounts

Set up a joint checking account for shared expenses. Ensure both partners have equal access and online banking capabilities. Maintain your separate personal accounts.

2. Discuss and List Shared Expenses

Identify all expenses that will be paid from the joint account. Common shared expenses include:

- Rent or mortgage payments

- Utility bills

- Groceries and household supplies

- Joint debt repayments

- Insurance premiums

3. Determine Income Contributions

Decide how income will flow into the joint account. Options include:

- Depositing entire paychecks into the joint account

- Contributing a percentage of income based on individual earnings

- Setting fixed amounts to cover shared expenses

4. Establish Guidelines for Surplus Funds

Agree on how to handle surplus money in the joint account. Choices involve:

- Saving or investing towards joint financial goals

- Equally dividing surplus into personal accounts

- Allocating extra payments towards shared debts

5. Define Non-Shared Expenses

Clearly outline what constitutes personal expenses. This may include:

- Personal hobbies and interests

- Individual subscriptions or memberships

- Supporting personal family obligations

6. Set Communication Protocols

Regularly discuss your finances. Schedule monthly or quarterly meetings to review joint account activity, adjust budgets, and discuss upcoming expenses.

Real-life Scenario: A Young Doctor and Pharmacist Implement the Method

Consider Sarah, a resident physician, and Mark, a pharmacist. They recently married and are navigating their combined financial landscape.

Their Financial Profiles

- Sarah: Has significant medical school debt and a modest residency income.

- Mark: Has a stable income with manageable student loans.

Applying the Separate + Joint Method

They decide to:

- Deposit their paychecks into the joint account to cover shared living expenses.

- Allocate surplus funds towards paying down Sarah’s high-interest student loans, viewing it as a joint goal.

- Maintain separate accounts for personal spending, allowing each to manage individual hobbies and discretionary purchases.

- Regularly review their financial plan, especially as Sarah progresses in her career and their income dynamics change.

This approach enables them to tackle shared financial goals while respecting their individual financial needs.

Tips for Success with the Separate + Joint Method

Prioritize Open Communication

Transparency is key. Regular discussions about finances prevent misunderstandings and keep both partners aligned.

Adjust as Life Changes

Your financial situation will evolve. Be prepared to revisit and adjust your approach as careers advance, incomes change, or new goals emerge.

Seek Professional Advice

Consider consulting a financial advisor who understands the unique challenges of healthcare professionals. They can provide personalized guidance on investment strategies, debt management, and financial planning.

Respect Individual Financial Goals

Each partner may have personal financial aspirations, like further education or starting a private practice. Supporting these goals strengthens the partnership.

Stay Informed About Financial Matters

Educate yourselves about financial planning for physicians or money management tips for doctors. Knowledge empowers you to make informed decisions together.

Conclusion: Building a Financially Sound Future Together

Marriage is a partnership that extends into all facets of life, including finances. The Separate + Joint Method offers a balanced approach for young healthcare professionals navigating the complexities of married finances. By fostering both collaboration and independence, it accommodates individual financial responsibilities and shared goals.

Embracing this method can lead to a harmonious financial relationship, allowing both partners to thrive personally and professionally. As you embark on this journey together, remember that flexibility, communication, and mutual respect are the cornerstones of financial success in marriage.

“`

Finding the Right Financial Advisor: A Guide for Young Healthcare Professionals

“`html

Finding the Right Financial Advisor: A Guide for Young Healthcare Professionals

As a young healthcare professional stepping into the world of medicine, dentistry, pharmacy, physical therapy, or psychology, your primary focus is naturally on your patients and advancing your career. Yet, with the increasing complexity of financial planning, investment management, and wealth preservation, finding the right financial advisor has never been more important. This guide aims to help you understand what to look for in a financial advisor and how to build a lasting relationship that supports your personal and professional financial goals.

Understanding Your Financial Needs

Before you start searching for a financial advisor, it’s crucial to assess your own financial situation and goals. Are you looking to manage student loan debt, save for a home, invest for retirement, or plan for a family? Young physicians and other healthcare professionals often face unique financial challenges, such as high educational debt and delayed entry into the workforce.

Common Financial Goals:

- Debt Management: Strategies to pay off student loans efficiently.

- Investment Planning: Building a diversified portfolio to grow wealth.

- Retirement Savings: Starting early to maximize compound interest.

- Tax Planning: Minimizing tax liabilities through smart financial decisions.

- Insurance Needs: Protecting income with disability and life insurance.

What to Look for in a Financial Advisor

Choosing a financial advisor is a significant decision that can impact your financial well-being for years to come. Here are key factors to consider:

1. Credentials and Experience

Look for advisors with reputable certifications such as Certified Financial Planner (CFP) or Chartered Financial Analyst (CFA). Experience working with healthcare professionals can be a plus, as they will understand industry-specific financial challenges.

2. Fiduciary Responsibility

Ensure the advisor acts as a fiduciary, meaning they are legally obligated to act in your best interest. This reduces potential conflicts of interest and ensures unbiased advice.

3. Services Offered

Assess whether the advisor provides comprehensive financial planning, including investment management, retirement planning, tax strategies, and insurance recommendations.

4. Communication Style

Effective communication is essential. Your advisor should be approachable, responsive, and able to explain complex financial concepts in understandable terms.

5. Fee Structure

Understand how the advisor is compensated. Common models include fee-only, commission-based, or a combination. Transparency in fees helps you know exactly what you’re paying for.

6. Investment Philosophy

Align with an advisor whose investment approach matches your risk tolerance and financial goals. Whether it’s passive index investing or active portfolio management, their strategy should resonate with you.

The Importance of Long-Term Relationships

A financial advisor isn’t just for the moment; they’re a partner for your financial journey. Building a strong, long-term relationship can provide stability and confidence as your life and career evolve.

Consistency and Trust

Trust is the foundation of any advisor-client relationship. Consistent communication and transparency build this trust over time. Your advisor should keep you informed about your financial progress and any adjustments needed along the way.

Proactive Communication

Life is full of unexpected events—market fluctuations, career changes, personal milestones. A proactive advisor will reach out during these times to adjust your financial plan as needed.

Why Clients Switch Advisors

Understanding why some clients consider changing advisors can help you make an informed decision and avoid potential pitfalls.

Common Reasons for Switching:

- Lack of Communication: Infrequent updates or unresponsiveness.

- Mismatched Investment Philosophy: Strategies that don’t align with client goals.

- Fee Transparency Issues: Hidden costs or unclear fee structures.

- Life Changes: Significant events prompting a reassessment of financial needs.

By selecting an advisor who prioritizes these areas, you can foster a relationship that endures over time.

Steps to Finding the Right Advisor

Here is a step-by-step guide to help you in your search:

1. Start with Referrals

Ask colleagues, friends, or family members for recommendations, especially those in the healthcare field who may have similar financial needs.

2. Research Online

Use online resources to find advisors specializing in serving young healthcare professionals. Review their websites for information on services and philosophies.

3. Check Credentials

Verify their certifications and look for any disciplinary actions through regulatory bodies like the SEC or FINRA.

4. Interview Multiple Advisors

Schedule consultations to discuss your financial goals and assess how well you communicate with them. Most advisors offer a complimentary initial meeting.

5. Understand Their Approach

Ask about their financial planning process, investment strategies, and how they tailor their services to individual clients.

6. Evaluate the Fee Structure

Get a detailed explanation of all fees and expenses. Ensure there are no surprises down the line.

7. Trust Your Instincts

Choose an advisor you feel comfortable with and who demonstrates a clear understanding of your needs.

Maintaining the Advisor Relationship

Once you’ve chosen an advisor, nurturing the relationship is key to your financial success.

Regular Reviews

Schedule periodic meetings to review your financial plan and make adjustments as necessary. This keeps you on track toward your goals.

Open Communication

Keep your advisor informed about changes in your life, such as marriage, new job opportunities, or significant purchases. This information helps them advise you more effectively.

Feedback

Don’t hesitate to share your thoughts on the services provided. Constructive feedback can enhance the relationship and ensure your needs are met.

Conclusion

As a young healthcare professional, your time is valuable, and your financial future is important. Finding the right financial advisor can provide peace of mind and allow you to focus on what you do best: caring for others. By understanding your needs, knowing what to look for in an advisor, and fostering a strong relationship, you can navigate the complexities of financial planning with confidence.

Remember, the right advisor is out there—one who aligns with your values, understands your profession, and is committed to helping you achieve your financial goals.

“`

Building Financial Stability: Essential Financial Planning Tips for Young Healthcare Professionals

Building Financial Stability: Essential Financial Planning Tips for Young Healthcare Professionals

Congratulations on embarking upon a rewarding career in healthcare! As a physician, dentist, pharmacist, physical therapist, or psychologist, you’re stepping into a role that places you at the forefront of improving lives. While your profession focuses on the well-being of others, it’s equally important to prioritize your own financial health. Navigating the financial landscape can be challenging, especially with the unique circumstances that healthcare professionals often face. This comprehensive guide aims to provide you with the tools and knowledge to build a secure financial future.

Understanding Your Financial Landscape

Financial planning begins with a thorough understanding of your current financial situation. This involves more than just knowing your salary; it encompasses your expenses, debts, assets, and financial obligations.

Assessing Income and Expenses

Start by itemizing all sources of income:

Primary Salary: Your base pay from your employer or practice.

Overtime and Bonuses: Additional earnings from extra shifts, performance bonuses, or incentives.

Side Gigs: Income from consulting, teaching, or writing.

Next, track your expenses meticulously:

Fixed Expenses: Rent or mortgage payments, insurance premiums, loan repayments.

Variable Expenses: Utilities, groceries, transportation, entertainment.

Periodic Expenses: Annual subscriptions, professional association fees, continuing education costs.

Utilize budgeting apps or spreadsheets to keep an accurate record. Understanding where your money goes is crucial for effective financial planning.

Managing Student Loan Debt

It’s no secret that many healthcare professionals graduate with substantial student loan debt. Managing this debt is often one of the biggest financial challenges.

Exploring Repayment Options

Standard Repayment Plan: Fixed payments over a 10-year period. While payments may be higher, you’ll pay less interest over time.

Graduated Repayment Plan: Starts with lower payments that increase over time, suitable if you expect your income to rise.

Income-Driven Repayment Plans: Payments are adjusted based on your income and family size, which can help manage cash flow in the early years.

Loan Forgiveness Programs

Investigate loan forgiveness opportunities:

Public Service Loan Forgiveness (PSLF): Offers forgiveness of remaining loan balance after 120 qualifying payments while working for a qualifying employer.

National Health Service Corps (NHSC) Loan Repayment: Provides loan repayment assistance to healthcare professionals working in underserved areas.

State-Specific Programs: Many states offer loan forgiveness or repayment assistance for healthcare professionals. Research programs available in your state.

Refinancing and Consolidation

Refinancing your student loans can potentially lower your interest rate, reducing the total amount paid over the life of the loan. However, be cautious as refinancing federal loans with private lenders may result in losing federal protections and benefits.

Establishing Financial Goals

Setting clear financial goals gives direction to your financial planning efforts. Goals should be SMART: Specific, Measurable, Achievable, Relevant, and Time-bound.

Short-Term Goals (0-3 Years)

Building an Emergency Fund: Aim to save three to six months of living expenses. This fund acts as a financial safety net for unexpected expenses or income disruptions.

Paying Off High-Interest Debt: Prioritize debts with the highest interest rates, such as credit cards or personal loans.

Savings for Major Purchases: Plan and save for significant expenses like buying a car or making a down payment on a home.

Mid-Term Goals (3-10 Years)

Further Education: Saving for additional certifications or degrees can enhance your career and income potential.

Investment in Practice: If considering starting or buying into a practice, begin accumulating capital now.

Family Planning: Prepare financially for marriage, children, and associated costs like education savings.

Long-Term Goals (10+ Years)

Retirement Planning: Establishing a retirement savings plan early maximizes growth potential through compound interest.

Financial Independence: Aim for a point where work becomes a choice rather than a necessity.

Legacy Planning: Consider how you wish to pass on wealth to heirs or charities.

Budgeting and Cash Flow Management

A solid budget is the foundation of financial health. It ensures that you’re living within your means and allocating funds toward your goals.

Creating a Realistic Budget

Develop a budget that reflects your lifestyle and priorities. Employ the 50/30/20 rule as a guideline:

50% Needs: Allocate half of your income to essentials like housing, food, transportation, and healthcare.

30% Wants: Use 30% for discretionary spending—dining out, hobbies, vacations.

20% Savings and Debt Repayment: Dedicate this portion to savings, investments, and extra debt payments.

Automating Finances

Automate bill payments and savings contributions to ensure consistency and avoid late fees. Set up automatic transfers to savings and investment accounts on payday.

Monitoring and Adjusting Your Budget

Regularly review your budget to track progress and make adjustments as needed. Life changes like salary increases, family additions, or moving can significantly impact your budget.

Investing Basics for Healthcare Professionals

Investing is a powerful tool for growing wealth and achieving long-term financial goals. Understanding the basics helps in making informed decisions.

Understanding Risk and Return

Investments come with varying levels of risk and potential returns. Generally, higher risk equals higher potential return. It’s important to find a balance that aligns with your risk tolerance and investment goals.

Diversification

Diversifying your investment portfolio helps mitigate risk. This means spreading investments across different asset classes, industries, and geographies. Consider a mix of:

Stocks: Shares of companies that can offer growth potential.

Bonds: Debt investments providing regular interest income.

Mutual Funds and ETFs: Pooled investment vehicles offering diversification.

Real Estate: Physical property or REITs for income and appreciation.

Retirement Accounts

Maximizing contributions to retirement accounts is essential. Some options include:

Employer-Sponsored Plans

401(k) or 403(b) Plans: Tax-deferred accounts often with employer matching contributions—a valuable benefit not to be overlooked.

457 Plans: Available to some government and nonprofit employees, allowing additional tax-advantaged savings.

Individual Retirement Accounts (IRAs)

Traditional IRA: Contributions may be tax-deductible, and earnings grow tax-deferred.

Roth IRA: Contributions are made with after-tax dollars, but qualified withdrawals are tax-free.

Investment Strategies

Develop an investment strategy that aligns with your goals and risk tolerance. Common approaches include:

Passive Investing: Investing in index funds or ETFs that track market indices.

Active Investing: Selecting individual stocks or funds to try to outperform the market.

Dollar-Cost Averaging: Investing a fixed amount regularly, regardless of market conditions, to smooth out market volatility.

Tax Strategies for Healthcare Professionals

Understanding and implementing effective tax strategies can enhance your net income and accelerate wealth accumulation.

Maximize Tax-Deferred and Tax-Free Accounts

Retirement Accounts: Contributions to 401(k)s, 403(b)s, and Traditional IRAs reduce taxable income.

Health Savings Accounts (HSAs): Contributions are tax-deductible, grow tax-free, and withdrawals for qualified medical expenses are tax-free.

529 College Savings Plans: For those planning for children’s education, earnings grow tax-free when used for qualified expenses.

Understand Deductions and Credits

Potential tax deductions and credits include:

Continuing Education Expenses: Deductions for costs associated with maintaining or improving skills required in your profession.

Professional Fees and Memberships: Deductions for necessary expenses related to your work.

Home Office Deduction: If applicable, a portion of home expenses can be deducted.

Strategic Tax Planning

Timing Income and Deductions: Accelerate deductions and defer income to reduce taxable income for the current year.

Capital Gains Management: Hold investments for over a year to benefit from lower long-term capital gains tax rates.

Charitable Contributions: Donations to qualified organizations can provide tax deductions.

Consult with a tax professional to tailor strategies to your specific situation.

Protecting Your Income and Assets

Safeguarding against unforeseen events is a critical component of financial planning.

Insurance Coverage

Disability Insurance: Protects your income if you’re unable to work due to illness or injury. Consider both short-term and long-term policies.

Malpractice Insurance: Essential for protecting against legal claims related to patient care.

Life Insurance: Provides financial security for your dependents. Term life insurance is typically more affordable for young professionals.

Umbrella Insurance: Offers additional liability coverage beyond standard policies.

Estate Planning

Creating an estate plan ensures that your assets are distributed according to your wishes.

Will: A legal document specifying how your assets are to be distributed.

Trusts: Can provide control over asset distribution and potentially reduce estate taxes.

Power of Attorney: Assigns someone to make financial and legal decisions on your behalf if incapacitated.

Healthcare Directive: Details your preferences for medical treatment if you’re unable to communicate.

Balancing Lifestyle and Financial Goals

As a healthcare professional, it’s important to find a balance between enjoying the fruits of your labor and striving toward long-term financial security.

Avoiding Lifestyle Inflation

With increasing income, it’s tempting to elevate your lifestyle accordingly. Be mindful to keep expenses in check to avoid derailing financial goals.

Setting Realistic Expectations

Determine what truly brings value and happiness to your life. Prioritize spending on experiences and items that enhance your well-being.

Seeking Professional Financial Advice

While managing finances independently is possible, professional guidance can provide significant benefits.

Choosing the Right Financial Advisor

When selecting a financial advisor:

Look for Fiduciaries: Advisors legally obligated to act in your best interest.

Check Credentials: Seek out Certified Financial Planners (CFP) or other accredited professionals.

Assess Experience: Choose someone familiar with the unique needs of healthcare professionals.

Benefits of Professional Guidance

Comprehensive Planning: Advisors can help with budgeting, investing, tax planning, and more.

Objective Advice: Provides an outside perspective free from emotional biases.

Time Savings: Allows you to focus on your career and personal life.

Conclusion

Embarking on your career in healthcare is commendable and requires significant dedication. Applying the same commitment to your financial well-being will yield invaluable dividends over time. By understanding your financial landscape, setting clear goals, investing wisely, protecting your assets, and seeking professional advice when needed, you can build a robust financial foundation.

Remember, it’s never too early to start planning for your financial future. Each step you take today brings you closer to achieving financial stability and freedom, allowing you to focus on what you do best—improving the lives of others.

Take control of your financial journey and make informed decisions to secure a prosperous future.

Managing Financial Stress: A Guide for Healthcare Professionals

Managing Financial Stress: A Guide for Healthcare Professionals

As a physician, dentist, pharmacist, physical therapist, or psychologist, you’ve dedicated your life to improving the well-being of others. While your career brings immense satisfaction, it can also come with unique financial challenges. In times of economic prosperity, it’s easy to overlook potential financial risks and focus on minor concerns. However, staying vigilant about your financial planning is crucial, even when things are going well.

This article aims to help healthcare professionals navigate financial stress, prioritize their financial goals, and build a secure future. We’ll explore common financial pitfalls, strategies for effective wealth management, and tips to ensure your financial health is as robust as the care you provide to your patients.

Understanding Financial Stress in the Healthcare Profession

Financial stress can affect anyone, but healthcare professionals often face unique pressures. High levels of student debt, the costs of setting up a practice, and the responsibilities of patient care can all contribute to financial anxiety. Even in times of low unemployment and strong economic growth, these underlying issues can create a baseline level of stress.

The Illusion of Prosperity

When the economy is thriving, it’s common for individuals to assume that their financial situation is secure. This sense of security can lead to complacency, where minor financial issues are overlooked or perceived as insignificant. However, this mindset can be dangerous. Ignoring small financial problems can allow them to grow into larger, more challenging issues down the line.

The Concept of Lifestyle Inflation

Lifestyle inflation occurs when increased income leads to increased spending. For healthcare professionals who begin to earn more, there’s often a temptation to elevate their lifestyle accordingly. While it’s natural to want to enjoy the fruits of your labor, unchecked lifestyle inflation can hinder your ability to save and invest for the future.

Common Financial Pitfalls for Healthcare Professionals

Understanding the common financial mistakes made by healthcare professionals can help you avoid them. Here are some areas to watch out for:

Ignoring Student Debt: With substantial student loans, it’s crucial to have a clear repayment plan. Ignoring or delaying payments can lead to increased interest and long-term financial strain.

Insufficient Retirement Planning: Relying solely on a pension or not contributing enough to retirement accounts can leave you unprepared for the future.

Lack of Diversified Investments: Failing to diversify your investment portfolio can expose you to unnecessary risk.

Overlooking Insurance Needs: Adequate disability and life insurance are essential to protect your income and family.

Failure to Budget: Without a clear budget, it’s easy to overspend and lose track of where your money is going.

Strategies for Effective Wealth Management

Implementing sound financial strategies can help you manage stress and build a solid financial foundation. Here are some steps to consider:

Create a Comprehensive Financial Plan

Developing a financial plan tailored to your unique situation is the first step toward financial wellness. This plan should include:

Debt Repayment Strategy: Prioritize high-interest debts and consider refinancing options.

Investment Goals: Define short-term and long-term investment objectives.

Retirement Planning: Maximize contributions to retirement accounts like 401(k)s, IRAs, or other applicable plans.

Emergency Fund: Establish an emergency fund that covers at least three to six months of living expenses.

Budgeting and Tracking Expenses

Maintaining a budget helps you stay on top of your finances and identify areas where you can cut back. Utilize budgeting apps or software to track your spending and adjust as necessary.

Diversify Your Investment Portfolio

Diversification reduces risk by spreading investments across various asset classes. Consider investing in stocks, bonds, real estate, and other opportunities that align with your risk tolerance and financial goals.

Protect Your Income and Assets

Insurance is a critical component of financial planning. Ensure you have adequate:

Disability Insurance: Protects your income if you’re unable to work due to illness or injury.

Life Insurance: Provides financial support to your beneficiaries in the event of your passing.

Malpractice Insurance: Essential for safeguarding your professional practice.

Plan for Taxes

Effective tax planning can save you significant amounts of money. Work with a tax professional to explore deductions, credits, and strategies that can reduce your tax liability.

Seeking Professional Financial Advice

Given the complexities of personal finance, especially for high-earning professionals, consulting with a financial advisor can be invaluable. They can provide personalized advice on:

Investment Strategies: Tailored to your goals and risk tolerance.

Retirement Planning: Ensuring you’re on track to meet your retirement objectives.

Estate Planning: Protecting your assets and providing for your family.

Debt Management: Creating effective strategies to pay down debt.

When choosing a financial advisor, look for someone who understands the specific needs of healthcare professionals. Verify their credentials and ensure they act as a fiduciary, putting your interests first.

Maintaining Financial Wellness Amid Prosperity

Even when the economy is strong and your career is flourishing, it’s essential to stay proactive about your financial health. Here are ways to maintain financial wellness:

Avoid Complacency

Regularly review your financial plan and adjust it as needed. Life changes such as marriage, children, or a new job can impact your financial situation.

Continue Educating Yourself

Stay informed about financial matters. Read books, attend seminars, and follow reputable financial news sources.

Set New Financial Goals

As you achieve your initial goals, set new ones to strive for. This could include expanding your investment portfolio, purchasing property, or increasing charitable contributions.

Monitor Market Trends

While it’s important not to react impulsively to market fluctuations, being aware of economic trends can help you make informed decisions.

Balance Work and Life

Financial wellness isn’t just about money; it’s also about quality of life. Ensure you’re taking time to enjoy life and avoid burnout, which can have financial consequences.

Conclusion

Financial stress doesn’t have to be an inevitable part of a healthcare professional’s life. By staying vigilant, planning ahead, and seeking professional guidance, you can build a secure financial future. Remember that even in times of prosperity, proactive financial management is essential. Take control of your finances today to ensure that you can continue to focus on what you do best—providing exceptional care to your patients.

Your financial well-being is just as important as your physical and mental health. Start implementing these strategies now to reduce stress and achieve the financial peace of mind you deserve.

Unlocking Financial Success: How Young Healthcare Professionals Can Benefit from Working with a Financial Advisor

Unlocking Financial Success: How Young Healthcare Professionals Can Benefit from Working with a Financial Advisor

As a young healthcare professional—be it a physician, dentist, pharmacist, physical therapist, or psychologist—you’ve dedicated years to mastering your craft. The journey has been long and demanding, filled with rigorous education, residencies, and the start of a rewarding career. Amidst this busy professional life, managing personal finances might seem daunting. This is where a financial advisor can make a significant difference, helping you navigate the complexities of wealth management, investment planning, and long-term financial success.

Navigating Student Debt and Early Career Earnings

One of the most pressing financial challenges for young healthcare workers is managing substantial student loan debt. According to recent studies, medical school graduates often carry debt exceeding $200,000. Balancing loan repayments with the onset of a competitive salary requires strategic planning.

A financial advisor can assist in:

Developing a personalized loan repayment strategy.

Exploring loan forgiveness programs and refinancing options.

Maximizing disposable income without compromising lifestyle.

By creating a tailored plan, advisors help you take control of your debt while setting the foundation for future financial growth.

Tax Planning and Efficiency

Healthcare professionals often face complex tax situations due to high income levels, additional private practice earnings, or investment portfolios. Effective tax planning is crucial to retain more of your hard-earned money.

Financial advisors can provide guidance on:

Utilizing tax-advantaged accounts like 401(k)s, IRAs, and Health Savings Accounts (HSAs).

Planning for quarterly estimated tax payments to avoid penalties.

Leveraging deductions and credits specific to your profession.

Through strategic tax planning, you can enhance your savings and invest more towards your future goals.

Investing for Long-Term Wealth